![]()

Content

| Sommaire | ||||

|---|---|---|---|---|

|

Trademark principles

Cards issued by French banks are largely attached to the French Cartes Bancaires (CB) network but also to an international network (Electron, Maestro, Mastercard, Visa, etc.). This is what allows the cardholder to use his card abroad. There are other local networks that issue co-badged cards. In Belgium, banks issue cards that belong to both the Bancontact network and also Maestro or Visa.

![]() Note : there are non-co-badged cards for which the regulations do not apply.

Note : there are non-co-badged cards for which the regulations do not apply.

As soon as a business accepts cards from different networks, it must allow consumers to select the brand they prefer.

If, for example, the merchant accepts CB, Mastercard and Visa cards, then the co-badged CB / Visa and CB / Mastercard cards are concerned, and the merchant cannot impose his choice. On the other hand, he can select his preferred network, which will be used if the consumer does not wish to change.

![]() Note : the network through which transactions pass can influence the amount of commissions applied by the acquirer. We invite you to contact your purchaser for more information.

Note : the network through which transactions pass can influence the amount of commissions applied by the acquirer. We invite you to contact your purchaser for more information.

Implementation

At the level of each Monext Online contract, the merchant can configure:

- The activation of branding : This option must be enabled to comply with MiFID regulations;

- The choice of default network for each type of card (debit, credit, business). This makes it possible to choose on which network the transaction will pass when the consumer does not make an explicit choice.

If the option is enabled, the consumer's choice always takes precedence over the merchant's default.

Regarding the Wallet , the network used by the 1 st transaction determines that used for the following transactions.

When activated on a contract, the "brand choice" functionality applies to transactions initiated in WebPayment ( Web mode, payment page and / or registration of a card in the Wallet ).

The manual entry of transaction in the backoffice allows the choice of the brand.

For the other modes, the collection of the choice from the customer is the responsibility of the merchant :

- DirectPayment : payment or payment by wallet, creation / modification of wallet;

- Batch Interface : authorization request function.

Configuration

Web mode

Choice of default network

In the configuration screen of a payment method in the backoffice, the merchant defines brand to be used by default according to type of card.

Introduction to the concept of brand choice

Like most French bank cards, your credit card is certainly a CB card. What's more, it is surely backed by an international network such as Visa or MasterCard. Convenient when you are abroad. However, in France, where all CB merchants accept at least the CB, Visa and MasterCard networks, there should theoretically be a conflict between the French network and one of the other two. And neither the merchant nor you, participate in the resolution of the conflict by selecting one of the networks. So which one is chosen? Should not one be able to take the network of one's choice when possible? This is part of the 2016 Resolution of the European Payment Services Directive Version 2 (DSP2).

Current operation

CB credit cards backed by an international network such as MasterCard or Visa can operate on one of the two networks (CB or MasterCard / Visa). In addition, French CB traders must accept these networks. On the other hand, since the CB network has priority over the other, an international CB card (CB MasterCard or CB Visa) carrying out a transaction in France will be done automatically on the French network.

Note: this operation does not apply to "only" cards. These are cards issued in France with only the MasterCard or Visa application. In fact, even in France, the transaction will not be processed by CB.

Tomorrow, the carrier will choose

However in mid-2016, a European regulation will impose to leave the choice to the bearer. Thus he will be able to select the French or international network. In principle, it is difficult to criticize this possibility offered to the bearer when he contributes for a card with multiple brands.

However, this choice, as innocuous as it may be, can be fraught with consequences. If a priori, this should not change much (eventually) for the merchant about commissions (CIP for CB and CMI for MasterCard / Visa) following the cap on commissions; this could be more detrimental for the CB payment system and therefore the banks.

Indeed, for the common man or for those who do not have the chance to know this blog, MasterCard and Visa are better known brands than CB and therefore safer. It's a safe bet that they will choose international networks. According to our information, 65% of consumers with a credit card click on Visa or Mastercard when choosing the card on a payment page.

The Payline proposal

Payline allows:

- the merchant to define the brand to use by default in the Payline contract, with the mark to be used by default for each type of card and the possibility to let the buyer make his own choice (not possible by default);

- that consumer choice predominates;

- payments by wallet, then the choice of the merchant possibly modified by the purchaser, is stored in the wallet;

- that the transaction benefits from monetary and regulatory conditions related to the brand (% interchange, period of validity, management of outstanding payments).

This consists in proposing the choice of the brand to the consumer via the different payment interfaces:

- Tpev: authorization functions and portfolio creation functions;

- Backoffice: function to create a manual transaction;

- Web pages: payment page and registration page of a card in a wallet;

- Web service: payment via webpage of payment and by direct interface, creation / modification of wallet, payment, payment by wallet;

- Batch: authorization request function.

The means of payment concerned are the following:

Payment method

Possible choices

CB/VISA/MASTERCARD

CB/Visa ; CB/Mastercard

BCMC

BCMC; TEACHER

Payline configuration

Default choice of the trader

In the payline backoffice payment method setup screen, the merchant defines the brand to use by default based on the card type.

From the moment the choice of the merchant is configured, all the transactions are carried out with this default mark unless the consumer chooses another one.

Consumer choice

In this same screen, the merchant

activates, if he wishes,must activate the functionality to leave the choice to

theconsumer on

thepayment pages

Payline.

He may not offer it when this choice is made in his shop.

Brand selection made on Payline pages

Payline searches after entering the first 10 numbers of the card, the default mark chosen by the merchant and displayed on the payment page.

Payment page v2

The brand logo is displayed in the card number field. By clicking on the logo, a list appears the consumer can fall another brand.

Payment tickets in APIs

Brand selection made in the shop of the merchant

![]()

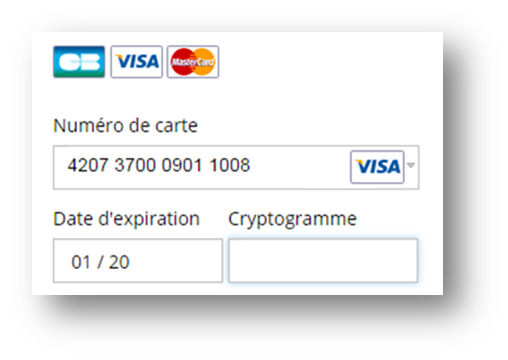

Brand choice on payment pages

When the consumer enters card number, the payment form will automatically offer the choice as soon as the card number is recognized as being co-badged.

The card logo is then transformed into a drop-down list, and the consumer can come and modify the default network.

![]() Note : If the merchant overloads the logos and / or user experience of payment widget, they must ensure that this does not alter the functionality.

Note : If the merchant overloads the logos and / or user experience of payment widget, they must ensure that this does not alter the functionality.

The payment receipt

The selected network is displayed on the ticket.

In DirectPayment mode

In the DirectPayment API mode, the merchant displays the payment form and collects the information from the consumer. It must offer a way to allow the consumer to select the brand (CB, Visa, Mastercard).

The Monext Online APIs can be used to pass information relating to the choice in order to comply with the banking protocol point of view with the acquirers.

The merchant sends Payline the choice made by the consumer during the payment request by fillingTo do this, the choice made by the consumer must be transmitted by filling

in the cardBrand field of the Payment and Wallet

itemsobjects with one of the following values:

- CB = 0

- VISA = 1

- MASTECARD = 4

- MASTER = 5

- BANCONTACT = 8

API webservices

Web service Monext Online |

Comments | |

Allow the merchant to transmit the brand to use ( |

cardBrand field ) It is only taken into account |

if the |

payment method allows the brand choice |

. |

If the payment. |

cardBrand information is not present, then |

Monext Online uses the default |

brand configured in the contract. |

Monext Online returns to the field: |

|

|

|

Monext Online returns the network to use in the network fields of extendedCardType and |

cardBrand |

of |

Monext Online allows the merchant to transmit the brand to |

be used ( |

payment.cardBrand field |

). It is only taken into account |

if the |

payment method allows the brand choice |

. |

If the payment . |

cardBrand information is not present, then |

Monext Online uses the default |

brand configured in the contract. |

Monext Online allows the transmission of the brand in the |

cardBrand wallet field |

It is only taken into account |

if the |

payment methode allows the brand choice |

. |

If the Wallet. |

cardBrand information is not present, then |

Monext Online uses the default |

brand configured in the contract. The response message is not |

changed. |

Same as createWallet. |

Monext Online returns the network to |

be used in the fields extendedCardType .network and wallet |

.cardbrand |

Monext Online returns the network to |

be used in the |

cardslist .cards and extendedCardType .network field |

Monext Online returns to the field: |

|

|

|

|

The

creation / modification screen ofscreen for creating / modifying a wallet obtained after

a call tocalling manageWebWallet

is modified at the entry level of the map coordinates as step 2 for the payment pages (widget and classic).supports the brand choice.

For recurring payments ( REC ), n times ( NX ) or wallet by web service, Monext Online

Recurring REC or NX payment or wallet payment via web service, Paylinesends the authorization request with the

data attached to the wallet.brand choice made during the 1st transaction.

Limitation and constraints

The customization of the logos of the means of payment is always possible but must not change the order for the payment pages v1.

Test card

The

card4974132154654656 card allows a

choiceCB /

VISAVisa choice by the buyer on the payment interface in an approval environment

of approval.